Why the continued rise of SIM only means we should be ready for a big quadplay push

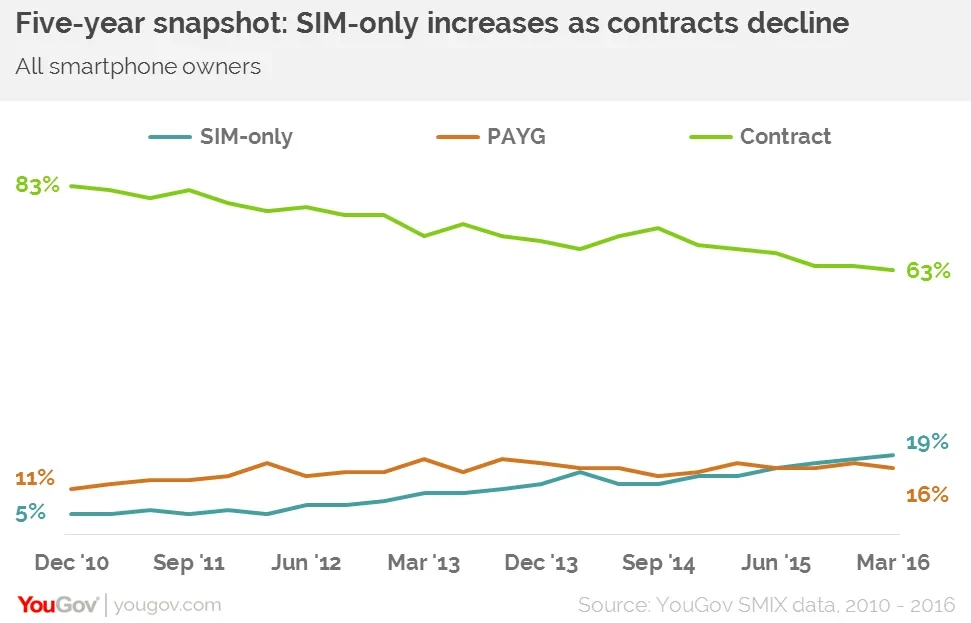

In the early days of smartphones dominating the mobile market, pretty much everyone had a contract. Back in December 2010 over eight in ten (83%) were tied to monthly bills with one in ten (11%) having pay as you go and just one in twenty (5%) chose SIM-only.

Five years ago each new iteration of a manufacturer’s centrepiece device saw consumers calling their network provider’s customer service line to change their contracts to get their hands on the latest model and its ground-breaking features.

But things have changed greatly and it has some very large ramifications for the mobile industry and beyond. Today, new device launches see incremental improvements meaning people are holding on to their phones for longer and running down their contracts. As a result, over a third of smartphone owners now are either on SIM-only deals (19%) or pay as you go (16%).

The Decline in the level of contracts has loosened the bonds of loyalty between consumer and network. Offering quadplay is one of the most likely ways to reverse this trend.

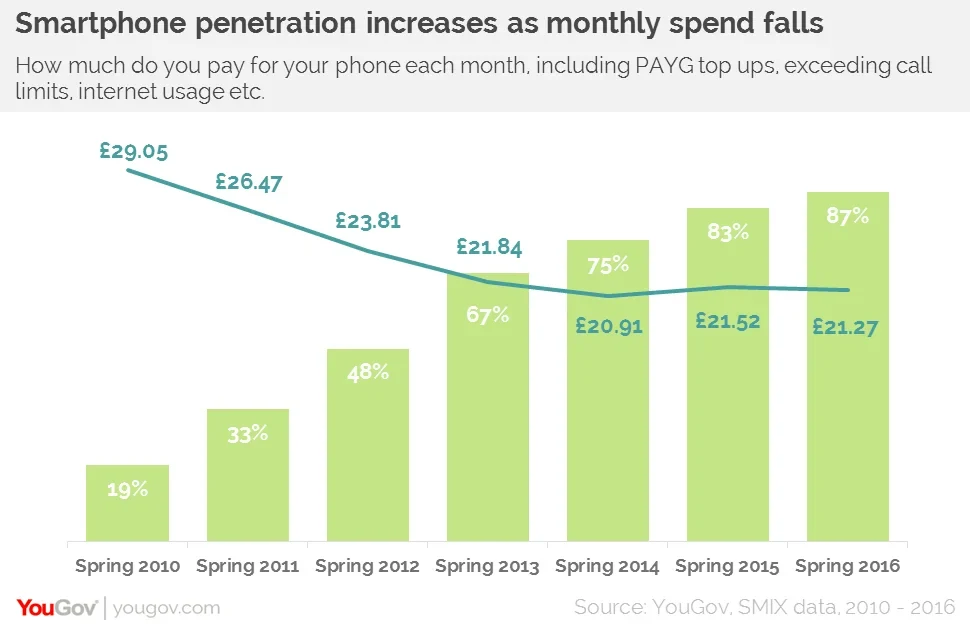

As smartphone penetration has increased the amount phone owners spend on their devices each month has declined. In the spring of 2010 almost one in five (19%) owned a smartphone and the average monthly spend was over £29 a month. Fast forward six years to this spring and 87% of phone owners have smartphone but they are spending just over £21 a month.

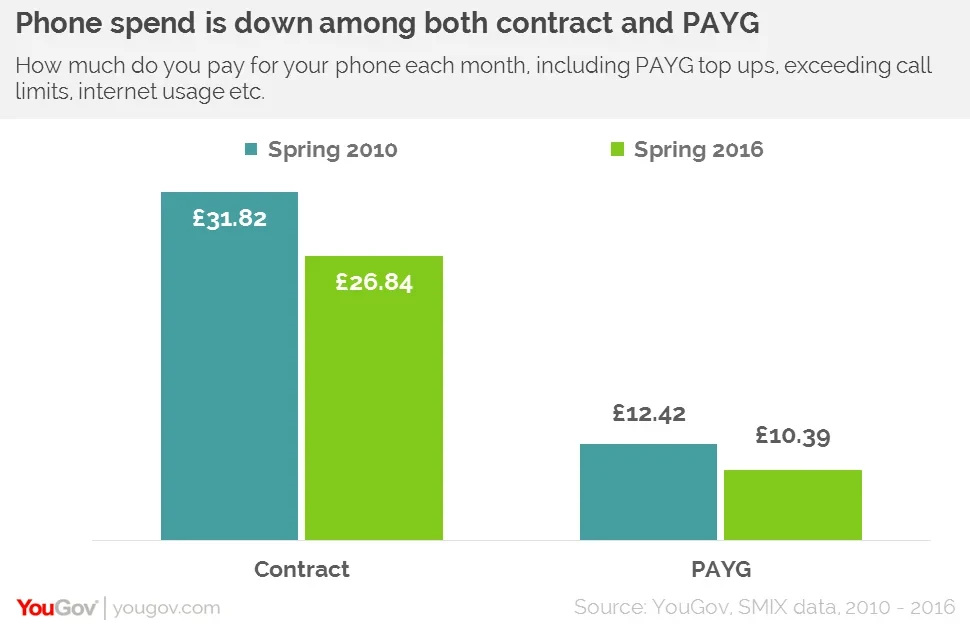

But it is not just the shift away from contracts that has affected the cost of running a smartphone and consequently operator revenues. In the past six years the average monthly amount paid by people with contracts has fallen from almost £32 to around £27 as the proportion of smartphone owners tied to a monthly bill fell. It is a similar story among those on pay as you go whose spend has decreased from £12 to £10 while the proportion of smartphone owners on PAYG has increased from 10% to 16%.

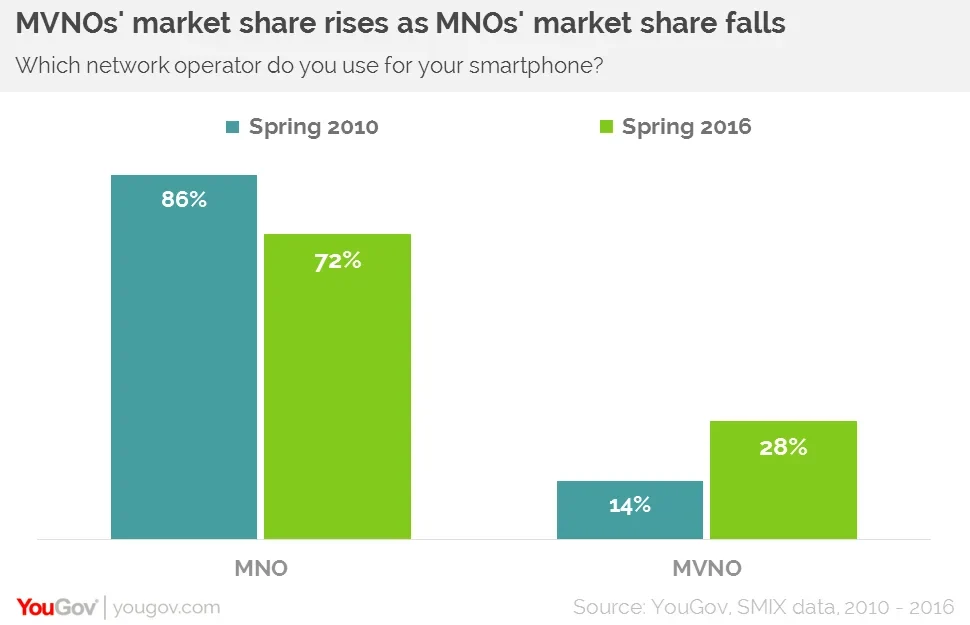

So is it a case of smartphone owners becoming more savvy, the deals now more consumer-friendly, or is there something else going on? It’s probably a bit of all three but one factor that can’t be ignored is that as there has been a drift to SIM-only and pay as you go deals, there has been a related move away from consumers using MNOs and towards MVNOs. In the past six years the proportion of smartphone owners on MNOs has declined from 86% to 72% with MVNOs growing as a consequence from 14% to 28%.

People are shifting because MVNO customers are more likely than MNO customers to choose their network provider because they are inexpensive (58% versus 15%). MVNO operators have also been boosted in recent years by offering high-end and mid-range handsets meaning they are picking up some phone aficionados from MNOs.

While all of this is interesting as of itself, the real significance lies in how brand loyalty among the bigger operators can be maintained and, if possible, restored. Offering quadplay is the centrepiece to this.

Among the 28% of smartphone owners who are with MVNOs, 11% are made up of quadplay providers, with Virgin (8%) and TalkTalk (2%) representing the biggest chunks. As the quadplay market develops, not only are these providers likely to grow further still but other operators are likely to offer mobile, landline, broadband and TV packages.

Several operators are already poised to cement their positions as quadplay providers. BT’s move from a MVNO to MNO further strengthens its offering as does the impending launch of Vodafone’s TV service as well as the recent launch of its broadband and landline service.

Given the decline in the number of people on contracts, the decrease in monthly spend and the shift away from MNOs, being able to offering consumers quadplay seems likely to help keep customers loyal to their chosen brand.

Image from PA