Sometimes sudden shifts in poll numbers matter less than the slow steady movements. Dramatic mood swings are liable to be reversed; gradual change is often sustained.

Want to receive Peter Kellner's commentaries by email? Subscribe here

This blog discusses a creeping change in attitudes that is invisible from week to week, and barely noticeable from month to month, but which could have huge ramifications for Britain’s politics in the years ahead. Slowly but inexorably, our gloom about our living standards has been lifting. It’s not that confidence has come roaring back. Pessimists still outnumber optimists. However, increasingly, we feel that the worst is behind us.

This is the consistent picture from three different sets of YouGov data: our measure of the “feelgood factor”, which we test each week for the Sunday Times; our monthly Prosperity Index; and our monthly Household Economic Activity Tracker (HEAT). (Full details of our HEAT and Prosperity Index data are available on subscription.)

Let us take each of these in turn.

1. Feelgood factor. Each week we ask: How do you think the financial situation of your household will change over the next 12 months? This is a question Gallup first asked in 1981, and which YouGov took over a decade ago. The following table shows how sentiment has changed since the start of 2011. (To iron out sampling fluctuations, I have averaged the four polls conducted in January 2011 and the three latest surveys.)

| % who expect their financial situation to... | Jan 2011 | April / May 2013 |

|---|---|---|

Improve | 8 | 12 |

Stay the same | 23 | 38 |

Total stay same / improve | 31 | 50 |

Get worse | 64 | 44 |

By historic standards, the feelgood factor is still weak, but it is vastly improved on where it was.

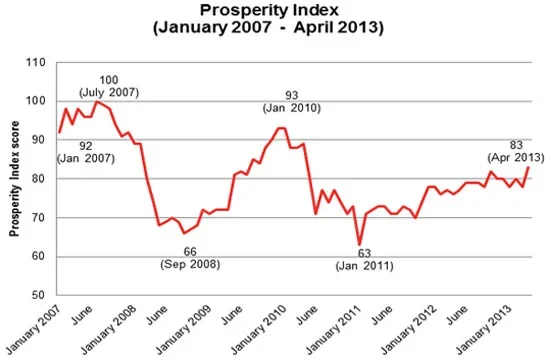

2. Prosperity index. Each month this combines responses to four different questions, of which the feelgood factor is one. The others concern satisfaction with living standards, plans to buy big-ticket purchases such as a television, computer or furniture, and (for working people) whether they expect the number employed at their workplace to rise or fall in the months ahead. The chart below shows how the overall index has moved since before Britain’s economy started to hit the rocks in 2007.

(Each question produces an index score. If positive answers match negative answers, the score is 100; the net difference between positive and negative moves the number up or down from 100; the overall index is calculated by adding the individual index scores and dividing the total by four.)

In July 2007 the index touched 100, for the first time since we started it in 2003. The economy was still growing, and Gordon Brown, the new Prime Minister seemed, for a very brief period, to get everything right. Then, at the end of the summer, the Northern Rock debacle saw people queuing round the block to get their money out, and confidence started to turn down, reach a low of 66 in September 2008, the month when Lehman Brothers collapsed. The index slumped from its highest ever figure to its lowest in just 14 months.

That was the nadir. Afterwards, as governments round the world stepped in to stop recession turning into depression, the mood started to brighten again. By January 2010, the index was back up to 93. It then reversed, with decline gathering pace after the general election and the austerity measures announced by the incoming coalition government. In January 2011, the index dipped even lower than it had in the wake of Lehman’s collapse; it stood at just 63.

Since then, the story has been one of recovery. The gradient has been gentler than that between 2008 and early 2010; some months have seen slight set-backs. But the direction of travel is clear; and the latest overall index, 83, is the highest since David Cameron became Prime Minister.

3. HEAT provides a much more detailed analysis of consumer sentiment, covering immediate behaviour, business activity, future prospects, house price expectations, job security and so on. This too has shown a gradual recovery since early 2011 to a post-election peak.

Both HEAT and the Prosperity Index suggest two main drivers of recovery. The biggest is house prices. Two years ago home-owners were fearful that the value of their biggest asset would decline. Those days have gone, at least for the time being: just 8% expect prices of homes in their area to fall over the next 12 months; more than 80% expect price stability or prices to rise.

The other driver is increasing job security. Subjective attitudes match the official employment data: despite the flat lining economy, more people are employed today than ever before. Of course this aggregate figure conceals a great deal of churn. Many jobs have gone. But whereas two years ago, millions of workers feared for their job, now those fears are less.

Not surprisingly London is leading the way. Its overall Prosperity Index now stands at 92, nine higher than the national average of 83; and it has risen slightly more than the rest of Britain over the past two years. But the bigger picture is that pessimism has declined across the board: in the North as well as the South, among those earning less than £20,000 a year as well as those earning more than £50,000; among those who live in rented homes as well as home-owners. Prosperity Index LEVELS continue to vary significantly from group to group; but the CHANGES are all in the same direction and roughly similar amounts.

All this should cheer the Conservatives. Should recent trends continue, and if Britain’s economy resumes steady growth, then this should help the party to persuade voters that their medicine is working. However, they should remember 1997. The Tories were thrashed, despite having presided over four years of vigorous growth, declining unemployment, rising living standards, low inflation and cheap mortgages. These counted for naught against the bitter memory of Black Wednesday five years earlier, when Britain was forced out of Europe’s currency club.

This suggests that to harvest the electoral rewards of a recovering economy, the Tories need to do something else. They must continue to persuade voters that our economic troubles were Labour’s fault in the first place, and fend of charges that the flat-ling of the past three years is George Osborne’s fault. Whatever happens to the economy in the run-up to the next general election, the contest to secure credit and deflect blame is far from over.

See the latest YouGov / The Sunday Times results

Learn more about YouGov's Household Economic Activity Tracker (HEAT)

Want to receive Peter Kellner's commentaries by email? Subscribe here