The retail investment market has been stifled for some time, with many consumers not willing or lacking the confidence to invest their savings for better long-term growth. However, as we emerge from the global pandemic and consumer confidence returns, many will have the potential to invest and may be tempted to look for better returns than current interest rates can deliver. Understanding consumer attitudes towards investing has never been more important.

Using YouGov Profiles, YouGov has developed a framework designed to help marketers better understand the portion of the British population with investable assets and their varying propensity to invest. It highlights the attitudes and behavioural traits of core consumer groups based on the value of the investable assets they have and the extent to which they look for profitable ways to invest money.

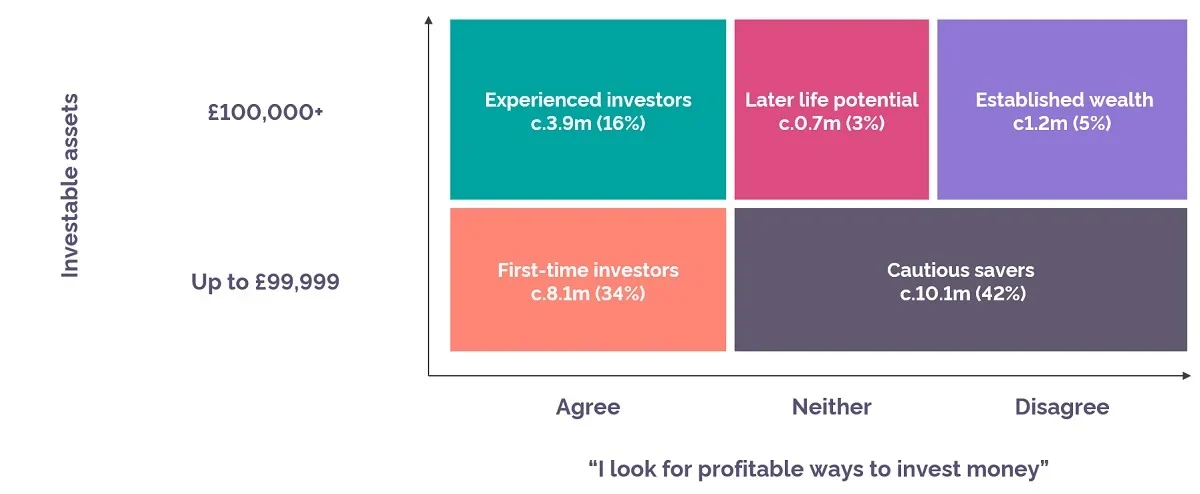

Before we go into further detail, here’s a quick glimpse at each segment:

Cautious savers: This group have a limited interest in investing and have investable assets of less than £100,000, representing 10.1m (42%) adults with investable assets.

Established wealth: This group have a high level of investable assets but are not interested in investing – representing 1.2m (5%) of adults with investable assets.

Later life potential: With assets worth £100,000 or more, this group is neutral on the question of investing it profitably. 0.7m (3%) adults with investable assets fall into this group.

First-time investors: This group have lower wealth but are looking for profitable ways to invest – making up 8.1m (34%) of adults with investable assets.

Experienced investors: The most willing and able group to invest their high worth, this group is made up of 3.9m (16%) adults with high amounts of investable wealth.

Cautious savers

This group makes up more than two-fifths (42%) of the GB population with investable assets. With no more than £99,000 worth of investable wealth, ‘Cautious savers’ are typically younger than the wider group. One-third of them (34%) are aged between 18-45 as opposed to 28% of consumers in the wider group.

As the title suggests, ‘Cautious savers’ are far more inclined to consolidate their wealth through more conventional methods of saving. While half of them (51%) say that saving for the future is their main priority, seven in ten (70%) find the idea of investing in stocks too risky. For marketers of investment instruments, there is perhaps an opportunity to appeal to this group by highlighting the higher returns possible from investing than a simple savings account.

Established wealth

The average consumer who fits the ‘Established wealth’ profile is significantly older than the average British adult. Over half of them (54%) are aged over 55 against just 38% of all GB adults. They are nine percentage points likelier than the national sample to have life insurance, and are roughly ten times more likely to be covered by income protection.

The reluctance to invest probably stems from the fact that this group already feels financially secure. For instance, half of them (48%), compared to nearly two in five (38%) nationally, say they don’t have a budget to manage their finances. Three in ten (29%) also say they aren’t saving for anything in particular. While this group appears to be the toughest sell for marketers, they make up only 5% of all adults with investable assets.

Later life potential

The demographic make-up of those in ‘Later life potential’ is close to that of the ‘Established wealth’ segment, with 63% of consumers aged over 55. In the same vein, almost half (49%) of them are retired compared to just one in four (24%) nationally.

Consumers in this category are twice as likely as the average Brit to have a premium bond (33% vs 15%). They differ from the ‘Established wealth’ category in that they are neutral in their attitude towards investment. This group, which represents strong potential for investment firms, constitutes 3% of all GB adults with investable assets.

First-time investors

One in three (34%) of the wider adult population with investable wealth fall into this group. This group is younger than the national sample – two in five (39%) are aged under 34, compared to 28% of all Brits. Notably, three-fifths (61%) of them are male, representing a 13-percentage point increase over the general adult population.

Over half (56%) of ‘First-time investors’ prioritise saving for the future and three out of ten are saving to buy a property or for a deposit. Along expected lines, consumers in this bloc are more tech-savvy. More than one-third buy financial products online, while one in eight (13%) refer to financial websites before making investments.

Experienced investors

This is perhaps the most-coveted segment for marketers of investment instruments due to its combination of high investable wealth and amenability to investing. This group makes up a sizeable 16% of all British adults with investable assets. Three-fifths (61%) of ‘Experienced investors’ are over 55 years old and two in five (42%) are retired.

Most notably, they are almost three times as likely as the average Brit to say they like taking risks in the stock market. One-third (33%) of ‘Experienced investors’ say they like to take risks in the stock market, compared to one in eight (12%) across all GB adults. One-fifth (19%) have a managed portfolio, compared to one in twenty (5%) nationally.