Retail veterans John Lewis and Waitrose announced plans for a significant management restructure this month. Come February 2020 the two businesses will completely merge their management teams.

The companies say the move isn’t designed just to cut costs but also “break out of the cycle of declining returns” of the sort that have led to multiple established retailers disappearing from the high street in recent years. Both John Lewis and Waitrose have themselves seen store closures this year.

YouGov data shows that the struggles experienced by both chains are very real, despite being very well established brands. John Lewis topped YouGov’s Brand Health Rankings this year ahead of Ikea and Marks and Spencer, meaning it’s the brand with the highest average of all BrandIndex’s tracking metrics, plus their Christmas advert is always eagerly awaited.

Despite this, John Lewis’s brand health score has declined in the past 12 months (from +42.1 to +41.3) alongside its value score (a net measure of whether consumers think the brand represents good or poor value for money) which has dropped from +22.1 in 2015/16 to +17.3 in 2018/19. The latter is a particularly worrying decline considering John Lewis’s ‘Never knowingly undersold’ promise.

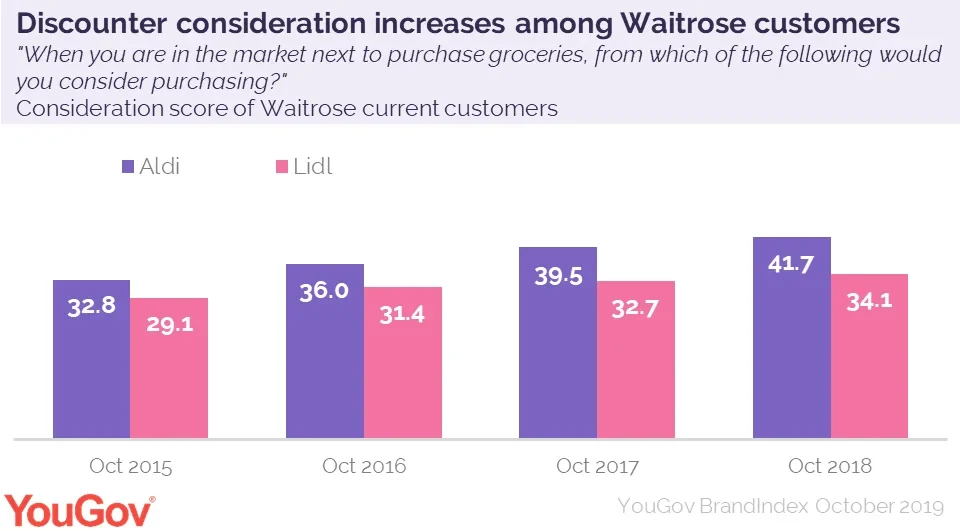

Similarly, Waitrose has experienced a decline in its brand health over recent years among its current customer base, from +77.5 in 2014 to +69.0 in 2019. Whilse perception of Waitrose had declined, Waitrose customer’s consideration (whether someone would consider purchasing from the brand in future) of major discounters Aldi and Lidl has improved significantly, highlighting the competition the supermarket faces.

It’s not just John Lewis whose value scores have fallen either – Waitrose’s declining value perception has led to customer perception falling which is important considering the emphasis that discounter brands place on value for money. Scores fell from +36.6 among current customers in 2015, to +20.8 this week.

It’s clear that John Lewis and Waitrose have experienced challenges over the past few years, whether due to the current climate or the arrival of impressive challengers. Whether this move to align the businesses will allow the brands to break this cycle is yet to be seen, however any move from such a long-loved brand that recognises the current strategy isn’t working is rather admirable.

This article previously appeared in City A.M.