The YouGov/Cebr Consumer Confidence Index has increased but at a much slower rate than we saw over the course of much of 2013.

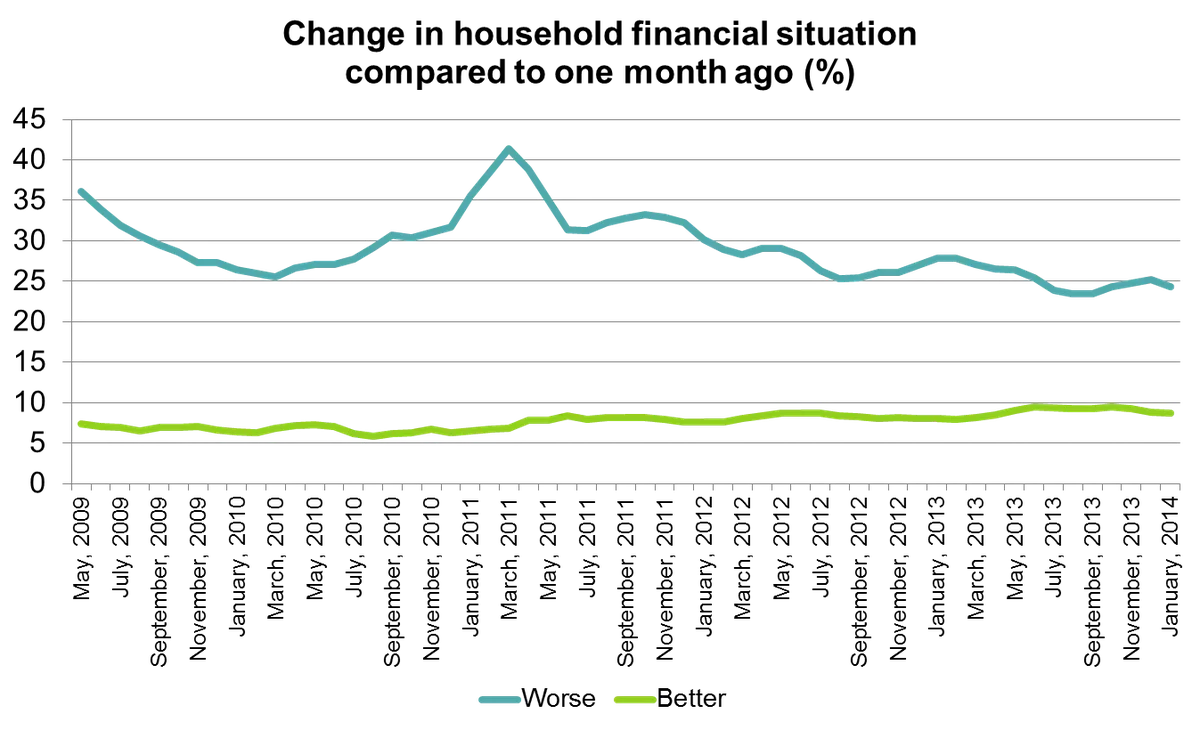

The underlying data suggesting that many consumers still aren’t feeling the benefits of the recovery in their pockets. Just 8.7% saw their household financial situation improve over the last month while almost a quarter (24.3%) said it got worse. However, consumers are marginally more optimistic about the future. The share of households expecting their financial situation to improve in the next 12 months increased by 1.3 percentage points compared to December – the biggest one-month rise since January 2010.

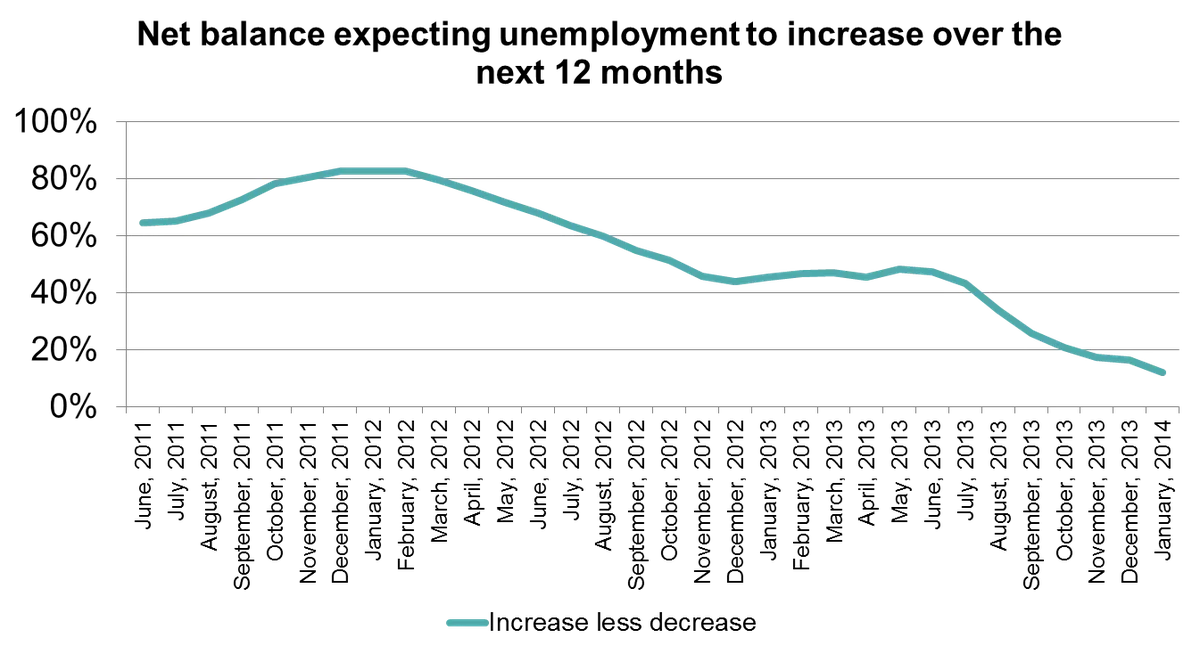

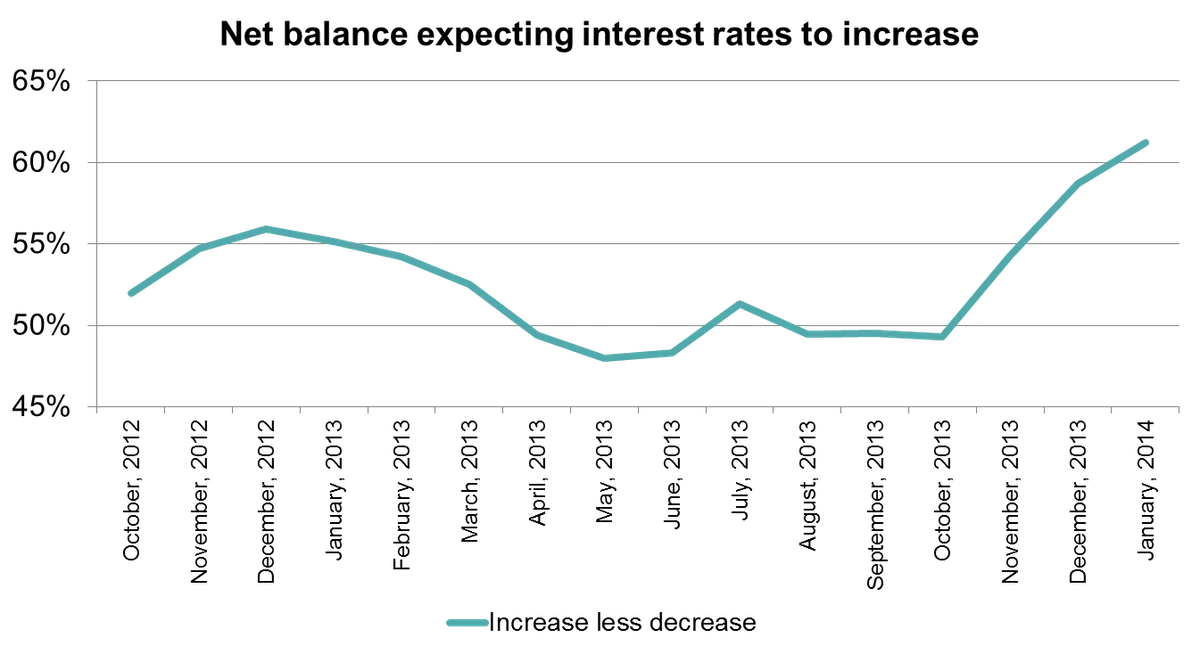

It comes as the spectre of unemployment fades from view. A net balance of just 12% expect unemployment to increase over the next 12 months, a fall of 70 percentage points since January 2012. Adjunct to this following the Bank of England’s Forward Guidance in the summer, a net balance of more than three in five people now expect interest rates to increase in the next year, a hike of almost 12 percentage points since Mark Carney made his announcement in August.

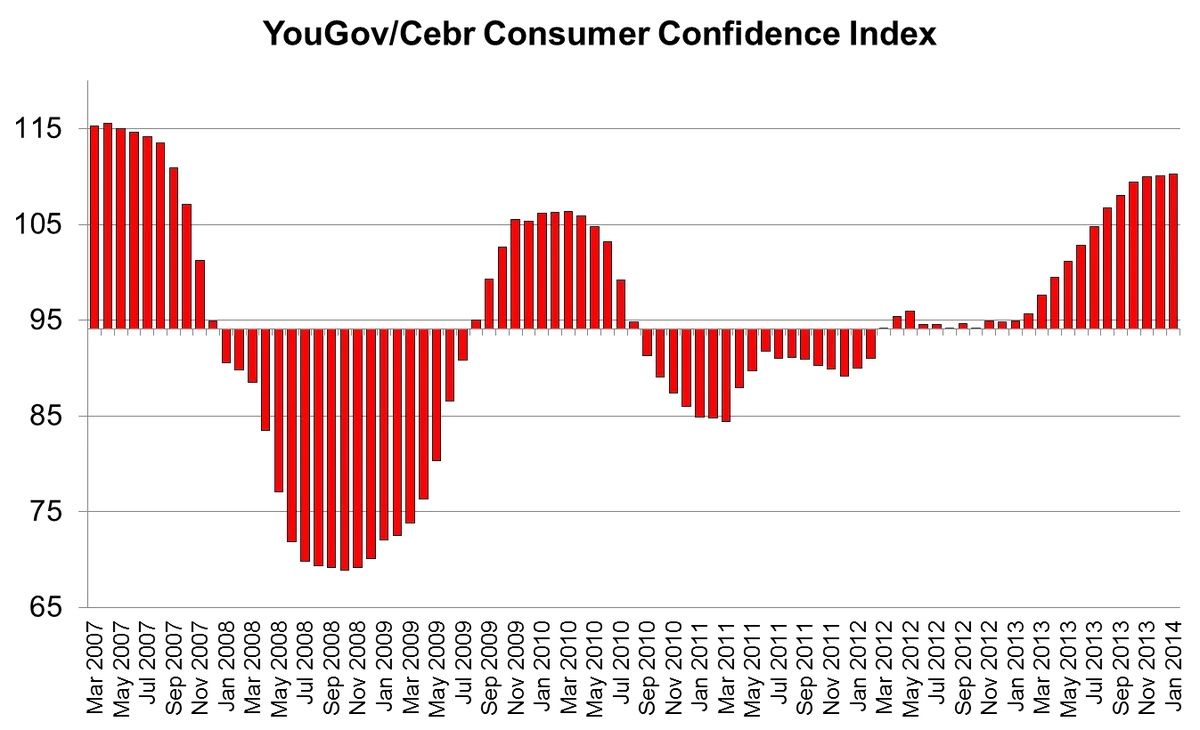

YouGov/Cebr Consumer Confidence Index

The YouGov/Cebr Consumer Confidence Index has improved to 110.3, its highest level since September 2007 when it was at 110.9. However, it is still well below its pre-crash level of 115.6 in April 2007.

The Index’s rate of growth slowed in Q4 2013 and the first month of 2014 in comparison to the increases seen in mid-2013. It has improved by just +0.9 points since the start of Q4 2013, a greatly reduced level of improvement when stood beside the +3.2 point growth it achieved over the course of Q3 2013 (from 104.8 to 108.0) and the +3.4 point increase of Q2 2013 (from 99.5 to 102.9).

Source: YouGov/Cebr HEAT data, January 2014, using a three-month rolling average.

Notes: Axis value of 94.1 represents the average HEAT Consumer Confidence measure since the data set began in 2007.

Household finances

Although the gap is narrowing marginally, the number of people who saw their financial situation deteriorate over the previous 30 days out-number those who saw them get better by almost three to one. Just 8.7% thought their household financial situation improved in the last 30 days compared to 24.3% who thought it got worse – a gap of 15.6%.

However, there are grounds for mild optimism. Over a fifth (20.3%) of people now think their financial situation will be better by this time next year, a month-on-month increase of +1.3%, the largest one-month improvement since January 2010 when it improved by +1.5%.

Source: YouGov/Cebr HEAT data, January 2014, using a three-month rolling average.

Unemployment

Despite ongoing pessimism over household finances, fears about unemployment are fading. Coming as the unemployment level falls to 7.1%, YouGov/Cebr’s figures show that a net balance of only 12.0% of people believe unemployment will increase over the next year – the lowest level since we began tracking this in 2011.In the past two years, concerns about unemployment fell from a high-point net balance of 82.6% in January 2012 to 45.5% in January 2013 and then decreased by -33.5 percentage points in the last year.

Source: YouGov/Cebr HEAT data, January 2014, using a three-month rolling average.

Interest Rates

Since the Bank of England’s Forward Guidance last summer, a fall in unemployment is joined at the hip to an increase in interest rates. Our latest data show that a net balance of more than three in five consumers (61.2%) now expect interest rates to increase over the next year, an increase of +11.9% from October when just under half (49.3%) thought they would go up in the coming 12 months.

Source: YouGov/Cebr HEAT data, January 2014, using a three-month rolling average.

Stephen Harmston, Head of Syndicated Reports at YouGov: ‘While they are optimistic about the economy as a whole, consumers are still pessimistic about their own circumstances. People’s household financial situations are slowly improving but so far the vast majority are failing to feel the benefits of the recovery while only a few see things improving. For optimism to spread, it needs to be felt in their daily lives.

‘The good news is that consumers no longer fear the spectre of unemployment. The bad news is that, despite Mark Carney’s shift away from the policy, Forward Guidance has made consumers concerned that a fall in unemployment will see a rise in interest rates which means higher mortgage payments. As far as a lot of people are concerned, the recovery is giving with one hand and taking away with another and this is why consumer confidence is static.’

Charles Davis, Associate Director at Centre for Economics and Business Research: ‘As the economy continues to strengthen and unemployment falls far sharper than the Bank of England expected, the one fly in the ointment is the continued weakness in pay growth. Our data show that consumers are still not feeling the benefit from the stronger economy. This may well start to change as the buoyant labour market eventually leads to pay increases through 2014. However, just as that potentially contributes to improving living standards, consumers fear an interest rate rise is ever closer although Bank of England Governor Mark Carney seems to be at pains to reassure that interest rates will stay low.’

Look here for more information about the The YouGov/Cebr economic briefing

Image from Getty