YouGov CEO, Stephan Shakespeare, suggests that Sainsbury’s Bank should capitalise on the positive perception held by its associated supermarket brand

Last week Sainsbury’s said that it had paid £248m to Lloyds Banking Group to take full ownership of Sainsbury’s Bank, buying out the 50 per cent stake owned by the lender.

Given what we know about consumer perception of these two brands, how might this move play out in the field of public opinion?

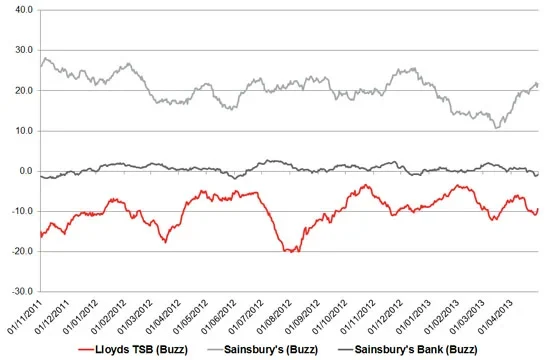

Looking at Buzz (whether people have heard positive or negative news about the brands) on YouGov’s BrandIndex, over the past 18 months we can see that Lloyds had a consistently negative score, varying between minus 3 and minus 20.

Meanwhile Sainsbury’s the supermarket had a consistently positive score, varying between +11 and +28, while Sainsbury’s Bank maintained a neutral score with very few people hearing about it either positively or negatively.

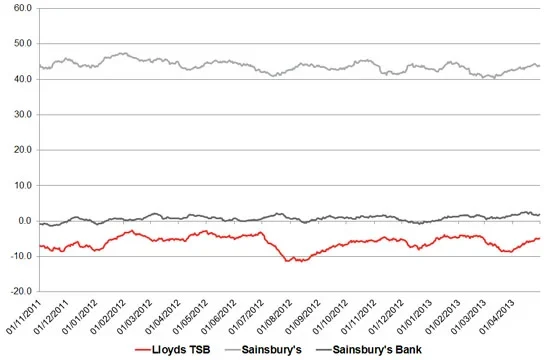

A similar but even more extreme pattern emerges when we turn to the Index score, a composite of six key image measures of brand health, which shows Lloyds around the minus 7 mark, while Sainsbury’s is one of the highest scoring brands, with an Index score consistently above +40.

Again, very few people have a view on Sainsbury’s Bank, leaving it with a score that tends to be close to zero.

So what does this mean for Sainsbury’s Bank, once it separates itself from Lloyds?

It has so far not really been able to capitalise on the reflected glory of its association with the popular supermarket brand, but equally it has not been tainted in the public eye by some of the issues that have beset the banking industry in recent years.

It should therefore take advantage of the fact that consumers have not punished it for its association with Lloyds (or for simply being a bank), and try to build on the glowing perception consumers have of its parent brand. If Sainsbury’s Bank can accrue even half the goodwill consumer have towards the supermarket, then it will lead the banking sector for consumer perception.