Four in ten (41%) don’t know how their pensions work – and one in ten (10%) don’t know what they’re contributing

Retirement is often portrayed as a well-deserved reward for a life of hard work: a time to take up bowls, go on cruises, and dote on grandchildren.

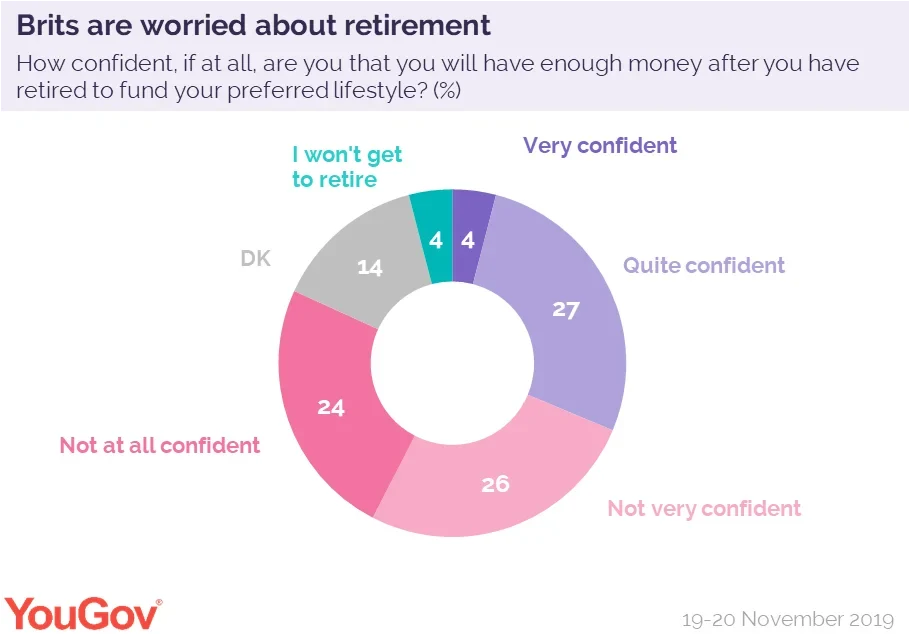

But new YouGov polling reveals that for many working Brits, it might be a more precarious proposition: fully half (50%) don’t believe they’ll have enough money to maintain their preferred lifestyle once they stop working. Two thirds (66%) also expect the state pension age to rise before they retire – with a third (33%) expecting it to significantly increase.

One in ten workers pays nothing into their workplace pensions

It’s clear that many Brits are pessimistic about their eventual retirement. This may be reflected in their attitude to workplace pensions.

Most importantly, four in ten (41%) working Brits don’t understand them at all. While over half (53%) say they do know how pensions work, almost half of women (49%) say they don’t compared to just over a third (34%) of men. This might not necessarily reflect a true gap in understanding: data from YouGov Profiles reveals that men are considerably more likely to describe themselves as “knowledgeable” than their female counterparts (58% to 43%).

More significantly, the largest group of working Brits – those aged 25-34 – are most likely to say they don’t comprehend pensions. Over half (54%) aren’t confident in their understanding compared to 39% of 18-24s, 40% of 35-54s, and 33% of over-55s.

That so many Brits don’t have a full grasp of pensions might expect why a tenth (10%) pay nothing into their pot, and another tenth don’t know if they’re contributing anything or not. Of course, the introduction of auto-enrolment for workplace pensions means that many of those who can’t say for sure if they’re contributing or not likely are – if only by default.

In fact, the default contribution is comfortably the most popular option among Brits in employment: over a third (37%) pay the minimum, while 27% pay more. Some 16% are self-employed or don’t have a workplace pension at all.

17% of Brits would withdraw money from their pension early if they could

Our survey also asked workers if they’d withdraw money from their pension pots before retirement – and overall, 17% are willing to take cash from their future selves.

Of this group, four in ten (42%) say they’d use it to pay for a large purchase such as a house deposit or a holiday, over a quarter (28%) say they’d withdraw the funds in emergency situations, and a fifth (21%) would use it for regular everyday spending. Those who would tap into their pension pot for day to day purchases are more likely to be in the NRS C2DE social grades than the ABC1s (25% to 18%).