Britons remain pessimistic while fears about the future grow, latest economic tracker reports

YouGov's latest Household Economic Activity Tracker (HEAT) shows that negative sentiment continues to prevail in the UK. The HEAT index is a monthly consumer sentiment number based on surveys conducted on a daily basis throughout the month.

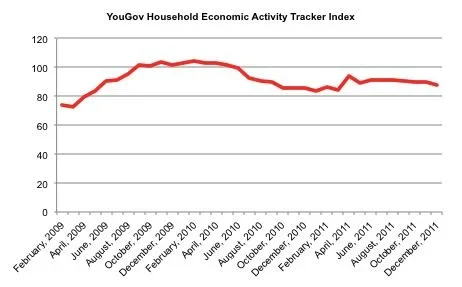

- The HEAT index remains low at 88 - negative sentiment prevails

- Unemployment remains a concern for Brits, with 28% identifying it as a major threat

- December 2011 saw a rise in household cash spend – well above December 2010 levels

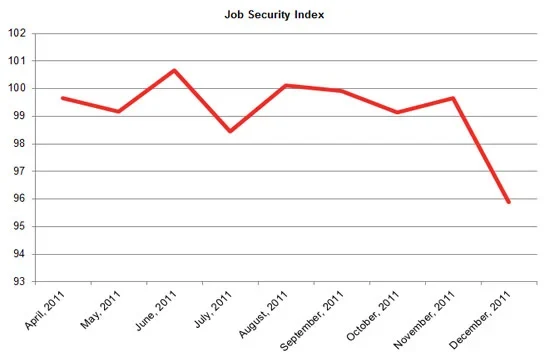

This month’s index score is close to the average index value for the past six months. In comparison, long-term job security index (respondents' estimate of the likelihood of their being laid off in next 12 months) has fallen to a new low of 96 among full and part-time employees (figure 2).

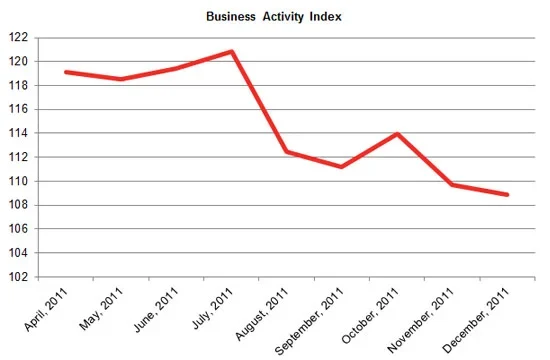

Simultaneously, however, within the private sector, the index measuring expectations of business activity in 12 months has dropped to 109 (figure 3).

Figure 1: UK HEAT Index

Index on scale of 0 to 200, in which 0 indicates entirely negative sentiment, 200 entirely positive sentiment, and 100 a balance of the two positions.

Source: YouGov Household Economic Activity Tracker, December 2011

Note: Based on interviews of 6,542 UK residents conducted from 1-31 December, 2011.

Index score is derived from consumer sentiment on 4 metrics (home prices, job security, family financial situation, and business activity) measured retrospectively and prospectively.

Figure 2: Expectations for future job security amongst full and part-time employees

Full- and part-time employees’ expectations for their future job security on a scale of 0 to 200, in which 0 indicates entirely negative sentiment, 200 entirely positive sentiment, and 100 a balance of the two positions.

Source: YouGov Household Economic Activity Tracker, December 2011

Note: Based on interviews of 1352 UK residents conducted from 1-31 December, 2011. Respondents were asked about the likelihood of being laid off in next 12 months, and could reply “Very Likely”, “Somewhat Likely”, “Neither likely nor unlikely,” “Somewhat unlikely,” or “Very Unlikely”. Each response was given a numeric score of 0, 25, 50, 100 and 200, respectively.

Figure 3: Expectations of business activity amongst private or self-employed workers

Private sector or self-employed workers’ expectations of future levels of business activity on a scale of 0 to 200, in which 0 indicates entirely negative sentiment, 200 entirely positive sentiment, and 100 a balance of the two positions.

Source: YouGov Household Economic Activity Tracker, December 2011

Note: Based on interviews of 1,352 UK residents conducted from 1-31 December, 2011. Respondents were asked whether they expect business activity at their place of work 12 months from now to be “Lower”, “Higher” or unchanged.

Holiday spending recovering

Whilst available spending cash remains roughly steady, December 2011 saw a rise in household cash spend that was close to levels observed in December 2009, and well above those in December 2010. Though UK households are still facing limited discretionary spending – with 8% having no discretionary spending available to them in December (in line with the average for the past 12 months) – their ability to increase spending over the holiday period shows that for some consumers the financial situation has become less dire.

To better understand how discretionary spend is changing, we asked UK consumers what they would do with a windfall of an additional month’s income (a leveling out in household finances is also suggested in consumers’ reactions to this question). The impulse to spend a windfall remains low at 13%, a rate at which it has idled for most of 2011. However, the percentage saying they would use a windfall to repay debts has fallen to 33% (from a high of 39% in August 2011) while those who would save the windfall has risen to 49%. This suggests that consumers are beginning to make a dent in their accumulated debts, but are not yet confident enough in their financial situations to start moving away from saving. Indeed, the percentage of consumers who would elect to save such a windfall is now at one of the highest levels it has been since data collection started in Feb 2009.

Home price confidence wobbles

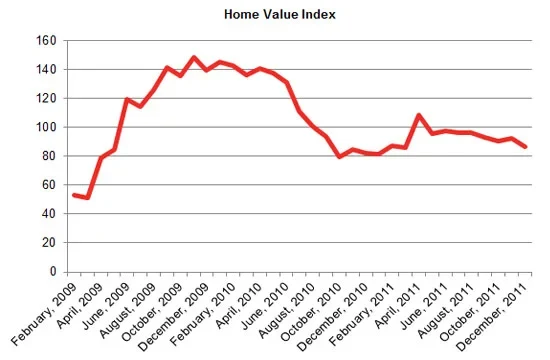

Home values are still seen as remaining steady or declining overall, with 58% of homeowners saying the value of their home has remained unchanged over the past month. At the same time, expectations of future property value increases amongst homeowners have again begun to sag. The index of homeowners’ expected changes in home value in 12 months’ time rose above 100 in mid-2011 but has fallen back to 87 in December (figure 4). The current trend appears to be toward increasing expectation of price stagnation in home values.

Figure 4: Homeowners’ expectations of the value of their home

Homeowners’ expectations of future value of their homes on a scale of 0 to 200, in which 0 indicates entirely negative sentiment, 200 entirely positive sentiment, and 100 a balance of the two positions.

Source: YouGov Household Economic Activity Tracker, December 2011

Note: Based on interviews of 2198 UK residents conducted from 1-31 December, 2011. Respondents were asked whether they expect the value of their home, 12 months from now, to be “Lower”, “Higher” or unchanged.

Continued fears of unemployment and recession

Unemployment has become the major concern for consumers, with 28% identifying it as a very major threat. This issue has steadily increased as a major concern over the course of 2011, up from 16% in early 2011. Inflation and energy price concerns (currently 16% and 24%, respectively) have both fallen substantially over the past quarter. At the same time, our Macroeconomic Sentiment tracker has shown a steady rise in expectation of Recession or Depression, with the former seen as the most likely outcome overall, with odds of 35%.

For more information on the HEAT please email our PR Executive, Giovanna Clark or call 020 7012 6069