YouGov CEO, Stephan Shakespeare, gives an insight into the latest consumer confidence figures

The latest figures from the YouGov/Cebr consumer confidence index show that the economic recovery is finally starting to move from a headline to a concrete reality for greater numbers of ordinary people.

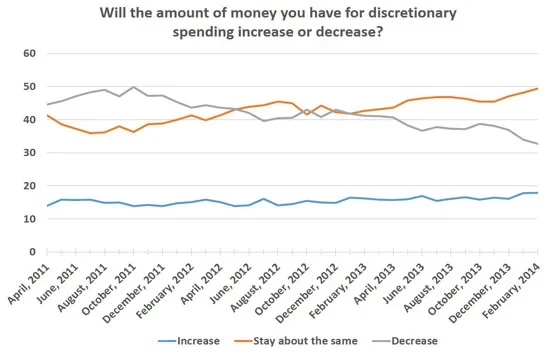

Champagne bottles are by no means being uncorked in large numbers, but there has been a steady increase in the percentage of people who say they expect to have the same (49 per cent) or more (18 per cent) money for discretionary spending over the next 12 months, while those who say they expect to have less have decreased from 41 per cent a year ago to 33 per cent.

One of the most oft-cited signs of recovery is the turbocharged UK property market. This week it was reported that the number of new mortgages being approved has reached its highest level for more than six years. In February, house prices rose by 0.6 per cent nationally – 2.1 per cent in London.

But while this might be good news for homeowners looking to sell, our research shows that it is not whether you own your home, but whether or not you live in London that most influences your economic outlook.

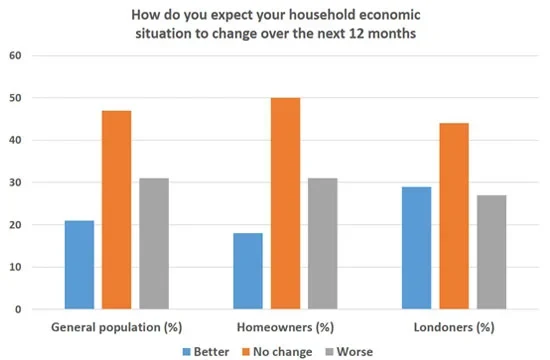

At a national level, significantly more people still expect their overall household financial situation to get worse, than expect it to get better (31 per cent versus 21 per cent). The view is no better for British homeowners, with only 18 per cent expecting their finances to improve, while 31 per cent think they will get worse. But for Londoners the situation is reversed, where more people (29 per cent) expect things to get better, and slightly fewer think they will get worse (27 per cent). For millions outside the capital, economic recovery is still just something they read about in newspapers. And the red-hot property market masks a much colder reality for many ordinary Britons.