The reputation of British banking was hit hard over the summer of 2012 as all four of the UK’s major high street banks generated some substantially negative headlines.

Libor fixing, computer glitches and money laundering all hit the papers, while mis-selling and foreign bailouts provided further mood music. It led to RBS Chief Executive Stephen Hester stating that banks had become “detached from society”.

YouGov research shows that Mr Hester’s comments are spot on and a gulf does indeed exist between customers and banks. While 42% of UK adults polled in August 2012 feel that “British banks can be good citizens”, bank reputations are at a very low ebb. Retail customers believe major banks have poor ethical and moral standards, have failed to learn the lessons of the financial crisis, and are treating their customers unfairly. Bankers’ bonuses in particular continue to rile, and have a corrosive effect on the reputation of banking beyond even the recent operational issues.

Summer of discontent

Reputation scores for individual banks fell considerably over what was a summer of discontent for the British banking sector as a whole. Individual banks were impacted by both their own issues and by those of their competitors, particularly around the Libor story. Barclays’ reputation in the mind of the UK public fell to a lower level than even BP experienced at the height of the Deepwater Horizon disaster in 2010. Trust in large banks was already low before summer 2012, but after it there remains a significant reputational gap between smaller and more trusted providers, such as The Cooperative and Nationwide, and the big four. HSBC comes closest to bridging this gap, with customer ratings well ahead of those enjoyed by RBS (NatWest/Ulster/RBS), Lloyds TSB and Barclays from their own customers. But these companies face major consumer concerns about their prudence and their financial stability.

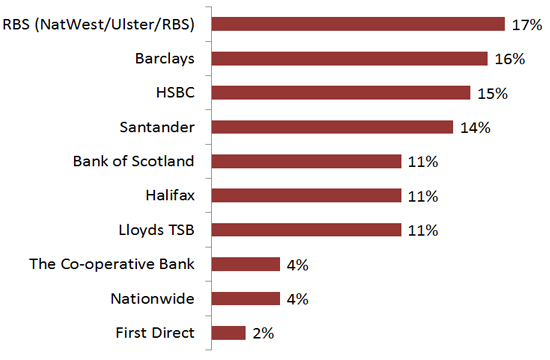

One way we can measure the impact these reputational issues have had on customer satisfaction is by the percentage of main account holders who say they are considering switching banks. Here we see that smaller providers like the Co-operative stand a far better chance of retaining their current customers, and will perhaps be the go-to for those customers fed up with their current bank

Proportion of main account holders considering switching to another bank

Path to rehabilitation

Despite their concerns, the public still believes the banking sector has a critical role to play in getting the UK economy back to growth. Nearly eight in 10 people (78%) in Britain believe that banks are critical to getting the UK economy growing again. This may offer a chance for the major banks to begin repairing their reputations, particularly if the process of “turning over stones”, as also mentioned by Mr Hester, is now complete and cultural change can be successfully delivered. An indication of the scale of the challenge that lays ahead for banks, however, is that an equal proportion (80%) of people say that the Barclays Libor scandal is symptomatic of a widespread problem of ethics in the UK banking industry.

Our research found that the top 10 things that build trust in a financial brand are:

- Behaving fairly and transparently with their customers 62%

- Good opinion given by friends and family 56%

- Knowing there is no risk of them going out of business 56%

- Offering consistent high-quality customer service 53%

- Rewarding loyalty 45%

- Only selling me things I need 45%

- Paying sensible bonuses to their staff/directors 38%

- Understanding my personal financial circumstances 36%

- They are well known 36%

- Being socially responsible 34%

At the heart of the problem is the fact that the public believes there has been a significant decoupling of the banks’ self-interest and the wider common good. Until customers believe that banks are again working for them and playing a positive role in the economy and society, they will remain cynical and mistrusting.

Though HSBC leads the big four by some way, there is clear evidence that other financial providers such as The Co-operative Bank and Nationwide all enjoy much stronger reputations than the big four on a number of measures. Combining the positive elements of these smaller organisations with the classic advantages that larger banks should enjoy can lay a platform for reputation growth which can be catalysed by the important role the banks need to play in the UK’s economic recovery.

See our related article on Banks: opportunity for rehabilitation.

If you have any enquiries please contact PR Executive, Harris MacLeod on +44 (0)2070126998.